In-depth analysis of the May 2025 non-farm report: Employment resilience supports economic expectations, gold is under pressure in the short term but still has opportunities in the long term

- 2025年6月10日

- Posted by: Macro Global Markets

- Category: News

The non-farm payrolls data for May released by the U.S. Department of Labor on June 6 showed that the number of new jobs was 139,000, slightly higher than the market expectation of 130,000, but slower than the revised 147,000 in April. The unemployment rate remained stable at 4.2% for the third consecutive month, in line with expectations. The wage growth rate exceeded expectations, with the average hourly wage increasing by 3.9% year-on-year and 0.4% month-on-month, indicating that labor cost pressures still exist.

2. Impact of the release of the small non-farm ADP data on the large non-farm market

In May, ADP private sector employment increased by only 37,000, the lowest level in more than two years, far below the expected 115,000, reflecting that trade policies have led to a significant decline in corporate recruitment willingness. After the release of the ADP data, the market's expectations for the big non-agricultural data were significantly lowered, the US dollar index fell in the short term, and gold rebounded due to rising expectations of interest rate cuts. However, the actual big non-agricultural data exceeded expectations and reversed market sentiment: the US dollar index soared 0.45% to 99.19, a nearly three-month high; the 10-year US Treasury yield jumped 11 basis points to 4.51%, indicating that the market's expectations for the Fed's policy shift have cooled.

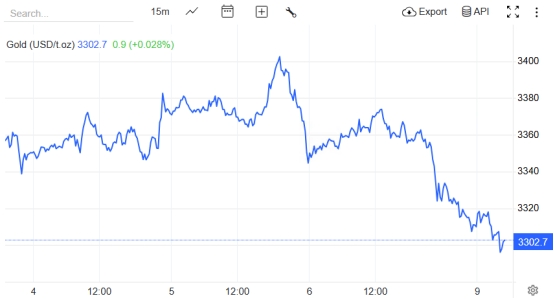

This expectation gap caused gold to fall rapidly after the release of non-farm payrolls, from an early high of $3,354/ounce to $3,307/ounce, and finally closed down 1.2%. The market logic shifted from "economic weakness → rising expectations of interest rate cuts → gold price rises" to "employment resilience → policy wait-and-see → gold price under pressure", highlighting the high volatility of market sentiment during data-sensitive periods.

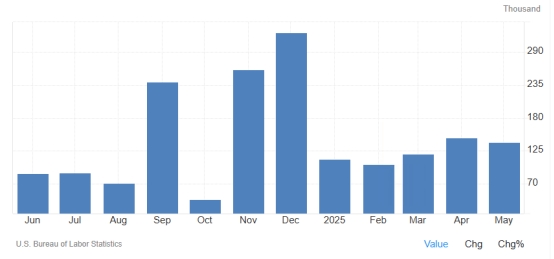

From the time series point of view, the US non-agricultural employment market shows a mild cooling trend:

May 2025: 139,000 new jobs (previous value: 147,000), unemployment rate 4.2%, hourly wage growth of 3.9% year-on-year.

April 2025: 147,000 new jobs (previous value: 177,000), unemployment rate 4.2%, hourly wage growth of 3.9% year-on-year.

March 2025: 120,000 new jobs (previous value: 185,000), unemployment rate 4.2%, hourly wage growth of 3.8% year-on-year.

New employment has been below 150,000 for three consecutive months, indicating a cooling of the labor market, but the unemployment rate remained low, reflecting that the contraction in labor supply may offset the impact of declining demand.

Although the hourly wage growth rate has declined slightly, it is still higher than the Fed's target, which has reinforced concerns about inflation stickiness and constrained expectations of interest rate cuts.

The data revision was significant, with non-farm data for March and April revised down by a total of 95,000, highlighting the lag and complexity of employment market statistics.

IV. Views of relevant institutions

Wells Fargo Group: The overall employment report is positive, indicating that the labor market remains solid. The stable unemployment rate and wage growth exceeding expectations may prompt the Federal Reserve to remain on the sidelines, and the probability of a rate cut in the short term is reduced.

ANNEX Wealth Management: The data appears positive on the surface, but details reveal problems, such as the extremely low manufacturing diffusion index, employment growth concentrated in a few industries, and questionable economic resilience.

CITIC Securities: Despite strong short-term data, the job market is still weakening. The Fed is expected to cut interest rates ≤ 2 times this year, which may be implemented at the September meeting.

Spartan Securities: The report has limited impact on the market. Although wage growth has attracted attention, it is not enough to change the Fed's policy path. Gold will be under pressure in the short term but will be supported by central bank gold purchases in the long term.

5. Gold price trend and future speculation after the release of the non-agricultural data

Short-term trend: After the release of non-agricultural data, the price of gold fell from $3,354/ounce to $3,307/ounce, closing down 1.2%, and the technical side showed a short position. The hourly level fell below the central structure, and the 15-minute level had strong downward momentum. The short-term support bit moved down to $3,270/ounce.

Upside risk: If subsequent economic data (such as CPI, PMI) show that inflation is falling or the job market is deteriorating rapidly, the expectation of interest rate cuts may be restarted, driving gold to rebound. The continuous gold purchases by global central banks (such as the Chinese central bank's seven consecutive months of reserve increases) provide long-term support for gold prices.

Downward pressure: If the Fed maintains its hawkish stance and the dollar and U.S. bond yields continue to strengthen, gold may fall to $3,200/ounce. In addition, a rebound in risk appetite (such as progress in trade negotiations) may divert safe-haven funds.

Risk warning: Geopolitical conflicts, the speed of the Federal Reserve's policy shift and the pace of global central bank gold purchases are key variables, and subsequent data and events need to be closely tracked.